Debt Action Plan: Simple Steps to Repair Credit & Reduce Costs

Discover a comprehensive Debt Action Plan designed to guide you on a transformative journey towards financial stability. With actionable steps to repair your credit, strategies to reduce your debt expenses, and tools to achieve freedom from debt faster, this guide is your roadmap to a secure financial future. Accompanied by a free PDF guide and budget spreadsheet, embark on a path to reclaim your financial independence.

(Click HERE to download a copy to read later)

Knowing were to start with taking action with your debt and making a plan that you will actually follow can be a real challenge, especially as we all have different circumstances and pressures in our lives; there is no “one size fits all” scenario here.

The following 4 stages will give you a good baseline for where you might want to start depending on which stage you identify with most strongly.

If you are already feeling overwhelmed and would prefer a simple checklist for your fridge or to keep on your desktop as a reminder, have a look at our free pdf download. Alternativly, take a look at our simple 7 steps to debt freedom guide that shows how to use all the free tools available in our free downloads section to get your plan together an tailor it to your needs.

If you are still confused, read on or take a look at our debt quiz.

Stage 1: Not too much debt and you’re managing the repayments easily.

– Extra money each month goes to pay off the outstanding capital.

– Credit score is looking good.

- Congratulate yourself on getting this sorted out now; if you were to leave it, these things can quickly spiral out of control.

- Check your credit score – make sure that all the information they hold about you is correct, you might have to get these things fixed before you move on.

- Make a clear record of how much you owe and what the interest rates are. If you know the charges each month but not the interest rates, take a look at our calculator HERE.

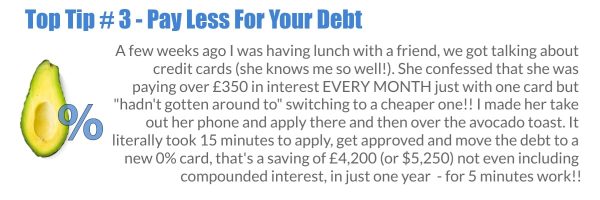

- See if you can get some 0% credit cards and use our excel tracker together with some FREE online loan calculators to see how this will affect your overall debt. Restructuring your debt so that you pay out as little as possible in charges is a really important first step. If you want more information on this look at our post on consolidation options.

- If you can’t switch your debts (either all or part of them) onto lower rate cards, pay as much as you can off the higher interest rate debts (use FREE online repayment calculators to see how this will benefit you long term)

- Do NOT jump into a consolidation loan or re-mortgage until you’ve exhausted the cheaper alternatives

- If you want to pay off debts even sooner, look at selling some unwanted items through eBay, amazon marketplace, Craig’s list, Facebook etc. Even downgrading your car or house might be an option if you are seriously committed!

- Reduce your outgoings by getting better deals on your household bills and regular spend items (Look at TopCashBack, Earny, Quidco, Shop at Home, to name but a few!) – see our post on how to use topcashback here – including how i’ve had over £1k back so far!!

- Start tracking your spend with a simple spreadsheet (see Debt Help Tools FREE downloads) or use an app (like Nitsova). hThere are so may free and realy user freindly options around these days, if you’re at home with this level of tech and the app your choose has all the right integrations with your accounts if could be a really quick win for you as far as tracking income, spend, creating budgets etc. is concerned.

- Check your insurances! Life, home, car, health etc, they all all worth checking and keeping track of renewal dates. Spend a day switching these over to cheaper and possibly better alternatives could save you $100’s over the year. Don’t forget to use comparison sites such as topcashback for even more money back on your switch. Some Utility and larger insurance campanies give you quite heafy lump sums just for switching to them.

- Don’t forget that government help is often available, especially in our current climate. It costs nothing to check and could be a total lifesaver!

Stage 2: A bit too much Debt but you’re still managing to make the minimum repayments.

– Paying off any larger sums is becoming more challenging though.

– Credit score has gone down a few points

- Don’t worry, you can do this!

- Check your credit score AGAIN! – make sure that all the information they hold about you is correct and that they have made changes that you asked for (if any)

- Make a clear record of how much you owe and keep it up to date, make a note of all the interest rates. Try using the Debt Help Tools FREE Debt Tracker for this.

- See if you can get some 0% or lower % cards or loans and use the FREE excel tracker together with some FREE online calculators to see how this will affect your overall debt.

- Making use of some the many budget apps available these days. These might also help you track your spend, especially helpful if you know this is a big issue for you.

- If you can’t switch your debts (either all or part of them) onto lower rate cards, pay as much as you can off the higher interest rate debts – look at DIY debt consolidation

- If you can’t see the situation improving in the near future, it might be time to start looking at a consolidation loan or re-mortgage if you are sure you’ve exhausted the cheaper alternatives. This option could be especially helpful if your main focus is to reduce your monthly outgoings on debt payments and are happy to pay a little more in interest to get this advantage. Whilst a consolidation shouldnt be your first point of call, if your interest rates are high and your credit score is passable, just improving your cashflow could be a huge win longer term.

- There are organisations out there that can get you Help to pay rent, which might be worth taking a look at.

- Don’t forget that government help is often available, especially in our current climate. It costs nothing to check and could be a total lifesaver!

Stage 3: It’s gone past manageable and it’s getting worse every month.

– You’re starting to miss payments and are getting really worried.

– Credit score is poor

- If you are really starting to NEED your debts paid off faster, maybe to look at selling some unwanted items through eBay, amazon marketplace, Craigs List, Facebook etc. Even downgrading your car or house might be an option if you are seriously committed!

- A re-mortgage or consolidation might be an option for you but do consider that as a mortgage is paid over the longer term, the traditionally lower interest rate has much more time to compound and has the potential to add up to quite a substantial sum. Take a look at our article on consolidation options to help you decide.

- Double check all your outgoings. Look at using an app like Nitsova or something similar that pulls all your spend into the app and shows you where it’s all going, as well as providing you with a trackable budget, this could be quite and eye opener! If this is a step too far, take a look at our free budget calculator in the form of a downloadable spreadsheet

- Check that you’re getting the best deal for all your usual spend like your utilities, phones, insurances, broadband, food etc. Make sure you are not paying for anything you don’t need. This is especially true with insurances. Life changes and you might be paying for cover that’s no longer relevant to you. Don’t forget to get extra back through cashback sites too! Remembering when these contracts are up for renewal is always a challenge i find! Often they end up autorenewing and we’re stuck in a contract that is either too expensive what what we need, or just not fit for purpose anymore. Try using a reminder sheet so you can get ahead of the curve next time around.

- Knowledge is key here. Debt can be incredibly stressful, especially if you don’t know what might happen, or what your rights are if you’re being hounded for payment. Check out this Debt Relief Manual, or take a look at “what lies in your debt”, alternativly look up some local debt charity organisations. Get informed about your options and what you can proactivly do right now to get out of your current circumstances. There is help available, you don’t have to suffer in silence or alone. It could also save you a fortune!

- Don’t forget, you can get Help to pay rent too and you could be entitled to a government grant which costs nothing to check.

Stage 4: OK so I think I’m in trouble now, I need help…. FAST!

Credit score is **!?*!

- Do not panic. Give yourself a pat on the back for facing up to this, you can do it!

- Take this slowly and methodically, you probably didn’t get here overnight so it might take a bit of time to get out of it, just one day at a time, one thing at a time………you will get there.

- Follow all the steps from the previous sections & look at opportunities to consolidate your debts into one place. If this isn’t getting you anywhere or you feel that you’ve exhausted all your options; then maybe it’s time for you to get in touch with a debt help organisation. It may even be worth contacting a specialist solicitor and getting advice on the various forms of insolvency or debt relief orders.

- If you are being hounded by creditors, get in touch with some debt charities in your local area. If there is a chance you are being pursued illegally, check out “what lies in your debt” to see if you could turn this around and MAKE money from your situation!

- Whilst bankruptcy or accessing some form of debt relief is definitely NOT something you should take lightly it could be the best solution for you at this moment in time so gather the information and make an informed decision.

- Don’t forget, you can get Help to pay rent too and you could be entitled to a government grant which costs nothing to check.

AT ANY STAGE, if it’s all too much & you just can’t cope!

If you are completely overwhelmed with it all and really can’t face dealing with it, that’s totally fine, but for your own health and wellbeing, and to enable you to fix your situation, you probably do need to address why you feel this way about money and possibly look at how your feelings about money and debt could have contributed to your current situation.

Money is still very much a taboo subject in most cultures so it often helps to speak to someone impartial that will not judge you but instead provide you will strategies to cope with your feelings around money and help you to help yourself create a better future.

Please do not despair, it’s just money and it can be fixed. Take care of yourself and take the process of sorting out your debts one step at a time. Don’t beat yourself up, just take each day as it comes, you will get there!

Why not pin this quick summary of the 30 step action plan so you can refer back to it anytime or check out our debt help guide for a more comprehensive view of your new debt action plan