-

-

-

Debt Help Guide

$0.99 -

The Tool Kit

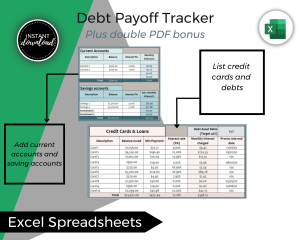

Debt Tracker Excel

- Track all your debts in one place and see at a glance which ones are costing you the most in interest.

- View your debt to asset ratio and your total monthly payments

- See how you can reduce costs by using your cash and assets that aren’t earning anything to pay down expensive debts.

The Tool Kit

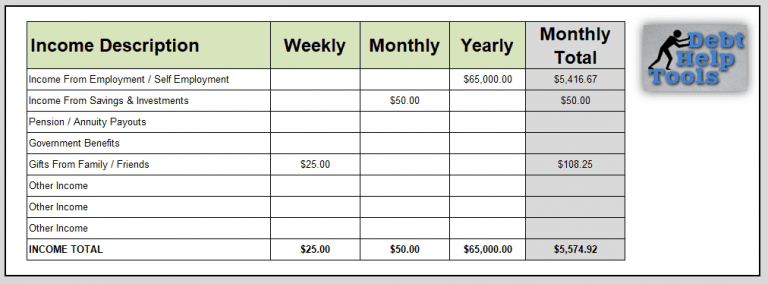

Monthly Budget Excel Spreadsheet Template

This Custom Budget Planner Takes Your Spend & Income & Instantly Shows You Exactly Where Your Money Is Going By Week, Month & Year – How Much You Really Need To Make Ends Meet & What You Can Do To Get Much More Out Of What You Already Have.

Plan Your Debt Exit

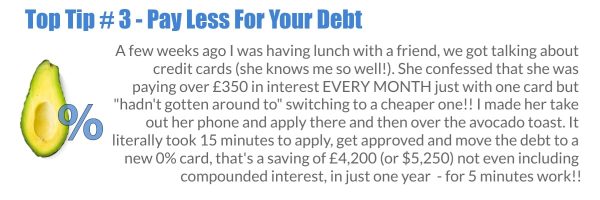

Simplify Your Debt: DIY Consolidation Methods That Save Money

Simplify Your Debt: DIY Consolidation Methods That Save Money Fancy paying one simple consolidated payment for all your debts without the high price tag? Get