How To Use Debt to MAKE Money

The principles of this are simple – take on good debt at a low interest rate and invest it into something that gives you a higher ROI, i.e. a higher interest rate – then you pay back the loan and keep the difference!

If however you are still in a lot of debt that’s charging huge sums of interest then please read “get out of debt fast” and look at my actions plans to help you get clear of BAD debt before you start looking at how to get and use GOOD debt to generate cash.

It can’t hurt to also check out your consolidation and bad debt options too if you’re really stuck and in need of a way out.

If however you have executed all the advice and resources available to you to optimise your income, minimise your outgoings and hopefully improve your credit rating, you can now start to use other people’s money to make some for yourself.

There is a HUGE caveat with this in that you really shouldn’t do it if you are not comfortable, you should also be very careful how you invest the money, keep the risk as low as possible which of course is always an important factor but it is especially so in this case as it’s not your money!

Taking on debt, any debt, even the lovely low cost, long pay back lead times kind of good debt, is always a risk so it’s really important to keep it balanced. If you ever owe more than you have in assets or savings then you are in debt.

Helping You With Long-Term Financial Goals

Remember – this is a business model not a licence to spend!!

As a disclaimer please note that this does not in any way constitute financial advice.

Before you do anything please get actual advice from an independent financial adviser. This tactic is just something I have employed in the past to make a little bit of extra cash and over the years I have found a number of other advantages in structuring my finances and using debt in this way, these include:

- Having available funds to take advantage of short term investment opportunities (e.g. short turnaround on tangible assets such as cars, real estate or auction items)

- Being prevented from going under or needing to borrow as a knee jerk reaction to demanding life events such as having kids or being out work through extended periods of illness

- Being able to muster deposits for houses in very short time scales

- Being able to maintain a decent credit rating despite how broke I am as I have never missed a payment – EVER!

- Getting better mortgage rates because I have a long term very good credit record

- Reducing my LTV on mortgages to get better rates whilst paying 0% on credit cards

- Being able to afford to develop properties by using cheap credit cards or loans to add value to them before i sell them on or let them out.

If you get this concept and you are comfortable with the management of it, you might want to think about how you can start to MAKE money by having debt and start things about the myriad of ways you can create value in existing or new assets, use the cash to generate income or simply invest in something that you know will produce a return before the debt has to be paid off.

Types of Debt

Good Debt vs. Bad Debt: In the realm of finance, the concepts of “good debt” and “bad debt” are often used to differentiate between types of borrowing based on their potential impact on an individual’s financial health.

Good debt is typically characterised as borrowing that can lead to an increase in one’s net worth or has the potential to generate income in the future. Examples include mortgages, where the property might appreciate in value, or student loans, which can pave the way for higher earning potential through advanced education.

On the other hand, bad debt refers to borrowing that doesn’t contribute to financial growth and often comes with high interest rates. This type of debt can quickly erode one’s financial position. Common examples include credit card debt accrued from frivolous spending or payday loans with exorbitant interest rates. While the distinction is clear in theory, in practice, the outcome of any debt often hinges on the borrower’s management and the broader economic context.

Taking on Good Debt and Cash Flow

Always keep in mind that this entire venture is about coming out of the end with MORE money than you went in with. If you take on a debt from a lender (even good debt) that suffocates your cash-flow and causes issues – expensive issues – in other areas of your life or business, then this entire endeavour could become a futile exercise. i.e. not worth the effort!

Debt CAN help a lot IF you can leverage it in the right way to make money with debt, but if the amount of debt that you take on or the cost of it does not tick the boxes on the ROI, then it can be really very bad for your personal finances, especially if you haven’t worked out your cash-flow properly and cannot repay.

When engaging in any business or financial endeavour, it is crucial to prioritise the goal of increasing your financial resources.

This means that any decision, including taking on debt, should be carefully evaluated to ensure it does not hinder your cash flow or create problems in other aspects of your life or business.

If the debt becomes burdensome and leads to costly problems, the entire venture may end up being a futile and not worth the effort.

Watch this video about cash-flow – it’s a great explanation.

Protect Your Credit Score

Please make sure that you:

- Don’t use more that 49% of your available balance

- Don’t apply for loads of new cards in a short period of time (too many HARD credit searches looks very bad!)

- Don’t take on more debt than you can service, i.e. you might be able to get $/£10k out of some existing and / or new cards on 0% but your minimum monthly payment to them would probably be about $/£200. Make sure you can afford this within your budget – defaulting would be a very very bad idea.

- Do set calendar and phone alerts for when the 0% runs out, letting these cards fall into interest charging instead of being the interest generators would not be good.

- DO invest the money safely; remember it’s not really yours.

Please do not start to feel like this is your money, it’s not as you have a debt for that same value. Don’t be seduced by looking at your credit balance and thinking that you have money: you don’t. Your saved money is like your employee that’s earning you an income via interest payments and it all belongs to your debt, not you. If you spend it, that’s like eating the golden goose and making a monstrous debt enemy at the same time.

The Simple Way to Use Debt to Build Wealth

In order to demonstrate the principle in the simplest possible way I am going to get in my time machine and go back a few years to when a savings account would pay you 5% interest on your money…….

2023 /24 looks like it’s going to be returning some similar rates but time will tell how cheap the debt will be!

I’ve discussed using 0% cards to pay off higher interest ones in some earlier posts.

If you’ve already done this or are debt free, you can now transfer a 0% card balance into your current account.

It is crucial to maintain a focus on financial gain throughout this endeavour.

Regardless of whether the debt is considered beneficial, it should not hinder cash flow or create problems that are costly for your personal life or business. Failing to consider these factors can render the entire venture pointless and not worth the effort.

How Debt Makes Money – The Case Study

As 0% options are become scarce these days you might have to substitute this for a “low rate” loan or credit card option.

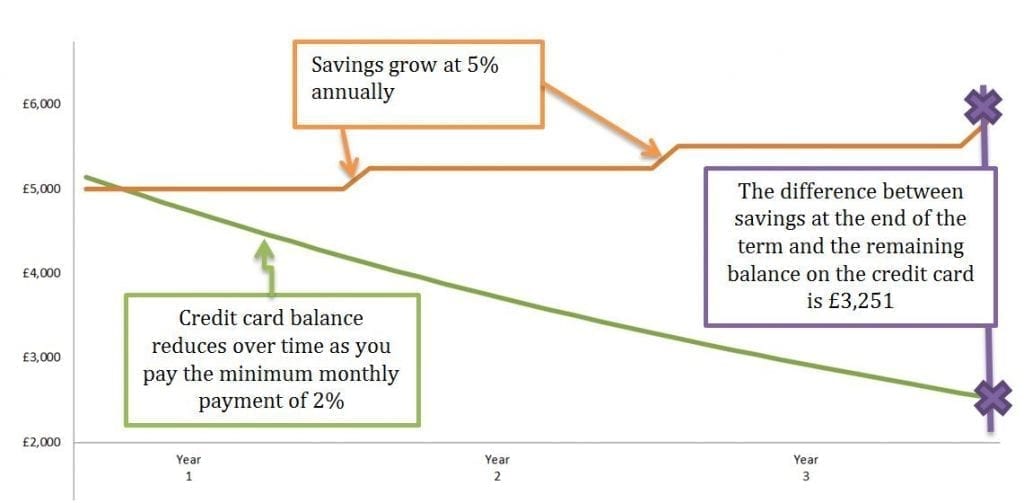

The following example shows how a 3 year 0% card with a 2.9% transfer fee on $5k might be used to earn $643 over the term.

So here you can see that you’ve taken $/£5k out on a 0% transfer for 3 years, you’ve paid $/£145 to transfer it and you’ve paid the minimum monthly repayments over the 3 years totalling $/£2,608.

This can of course apply this to any asset that you believe can return MORE from the investment in it than the cost of your loan or credit card interest rates or transfer fees.

When the 3 years is up, you liquidate your savings (total of $5,788), pay off the final balance on the card of $2,537 and bank the remaining $3,251 which; given that you paid into the credit-card over the year, provides you with a ….

…..total profit of $/£643 ($3,251-$2,608).

All from money that was never yours!

Tax On Your Profit

Please remember that you will have to declare this income for tax purposes but if your accountant does a good job you will be able to offset the original loan interest amount and maybe a few other things depending on your personal situation, your business structure, country of residence and the type of investment you decide to enter into.

Additionally, it is important to keep track of all expenses related to the investment, such as transaction fees, legal fees, and any other costs incurred. These expenses can also be used to offset the income generated from the investment and reduce your taxable amount.

It is advisable to consult with a professional tax advisor or accountant who is familiar with your specific circumstances and the tax laws of your country. They can provide guidance on how to accurately declare the income and take advantage of any potential deductions or credits available to you.

Remember, tax laws can vary significantly between countries and change regularly, so staying informed and seeking professional advice is crucial to ensure compliance and optimize your tax position.

Invest Debt to Build Wealth

To be clear, this is for investments not for spending on something that you intend to own and use for a long time such as a home of family car – these are not assets that return any value.

A house (or any other purchase for that matter) that you intend to rent out or by any other method, generate cash flow from however would be considered and investment as it would return income by way of regular payments and capital gains.

13 Steps To Turn Debt In To Profit – The ACTION Plan!

To summarise what we’ve covered:

Before You Start – Get Free from BAD Debt

- Get your head in the right place. Taking on debt is a risk and you shouldn’t do this if you already have loads of bad debts!

- Make the decision that you want to be debt free, be financially secure and build long-term wealth. Be very clear with yourself about how much you want it and remind yourself daily!

- If you are not fully committed to the decision; do some work on yourself to understand why. Examine the language you use when you speak about money and get to the root of your subconscious beliefs and expectations. Don’t skip this step!

- Read or listen to some books, blogs, podcasts or watch you tube, there is some amazing content out there these days and it’s mostly free so go and feed yourself with loads of good uplifting and sustaining beliefs. This is especially useful if you know you are surrounded by people who are a negative influence on you when it comes to your ability to handle money.

- Get a practical grip on all your debt, how much you owe, who to and how much it’s costing – and don’t panic, it’s still only money!

- Switch as much expensive debt as you can to 0% or low cost, if you can’t do this fully; get the next lowest possible, find some professional advice, look at debt charities and consider an IVA or bankruptcy if it’s really that bad, but again – don’t panic, there is always a way.

After the Bad Debt is Gone – it’s Time to Use GOOD Debt to Make Some Money!

(Good debt only comes to those with a good score!!)>

- Get your credit rating sorted and make sure that the information they hold about you is correct and keep it that way.

- Minimise outgoings and maximise income. You don’t have to achieve this all at once but have a timed plan of when you with take action on each step.

- Do one small thing every day that aligns with your new goals.

- Decide on the maximum monthly “payment” you can make to your “future you” pot. This might be for clearing debts or regular investment deposits, or both. Either way, decide what you can afford (at a stretch) and put it in a separate account.

- Finally get some free or really cheap debt (in line with what you can afford to service each month) and use that debt to buy assets at the lowest possible risk in a higher interest fund or account.

- Check weekly, then monthly to make sure it all stays on track

- Retire rich and happy!

Millionaires Use Debt To Make Money All the Time

If you remain unconvinced that using debt to make money is a real thing, watch this multi millionaire explain it……..

He, and many other successful business people have used low cost loans to leverage their finances to create wealth from a wide range of investments.

If you have ever read pretty much any of the money related book, they all speak about leveraging other peoples money, all I’m doing is using it on a much smaller scale.

Key Takeaways

- Profitable Debt Strategy: Borrowing money, especially at 0% interest, can be a strategic move when the borrowed amount is invested at higher returns.

- Good Debt vs. Bad Debt:

- Good Debt: This is debt that can potentially generate income or increase in value over time. Examples include mortgages (which can lead to property appreciation) or student loans (which can lead to higher earning potential).

- Bad Debt: This refers to debt that doesn’t improve your financial position and doesn’t provide a return. Examples include credit card debt from unnecessary purchases or high-interest loans without a clear return on investment.

- Learning from the Past: Learn from previous financial experiences, both personal and those of others, to prevent repeating common mistakes.

- Never Invest what you cannot afford to lose!